The $200M Brain, the $50K Body

Why Hyundai Won the Humanoid Race Before Anyone Noticed

THE LENS IN ONE PARAGRAPH

Atlas is not one robot. It is three stacks in a trench coat — cognition, embodied control, and actuation — each owned by a different company with a different economic curve. Google failed because it wanted the whole stack and had no factories. SoftBank failed because it wanted the whole stack and had no manufacturing. Hyundai won because it only needed one layer, and the part was already on the shelf. That is the lesson. Disaggregation is not a theory this month. It is the production-form of every humanoid that will ship in 2026.

The story everyone is telling

On January 5, 2026, at CES in Las Vegas, Boston Dynamics CEO Robert Playter announced that serial production of the new electric Atlas humanoid had officially begun. The 2026 production run is already fully committed — split between Hyundai’s Robotics Metaplant Application Center and Google DeepMind. Hyundai is putting roughly $26 billion into U.S. operations, including a factory designed to produce 30,000 Atlas units per year by 2028.

The narrative that has settled around this announcement is roughly the following: Boston Dynamics survived four ownership changes and finally found a patient parent. Hyundai got lucky with a prescient $880M acquisition in 2021. Tesla Optimus, Figure, Unitree, and Apptronik are about to get an uncomfortable Christmas.

All of that is true. None of it is the interesting part.

The story nobody is telling

The interesting question is not why Boston Dynamics took thirty years to ship a product. It is why Google and SoftBank — two of the most patient, best-capitalised technology investors in history — each held this asset for four years and each decided to write it off. Google paid roughly half a billion dollars for a robotics portfolio in 2013. SoftBank paid an undisclosed premium in 2017. Both of them, in turn, sold Boston Dynamics to a car company.

A car company.

If you squint at the industry press, the explanation you get is always the same: “Hyundai has factories and the others didn’t.” That is true, but it is not the explanation. Ford has factories. Toyota has factories. General Motors has factories. Every major automaker in the world has factories. Only one of them ended up owning Boston Dynamics, and that was after the field had spent ten years treating Atlas as a viral-video curiosity.

“Hyundai did not buy a robot. It bought a missing layer of its own stack.”

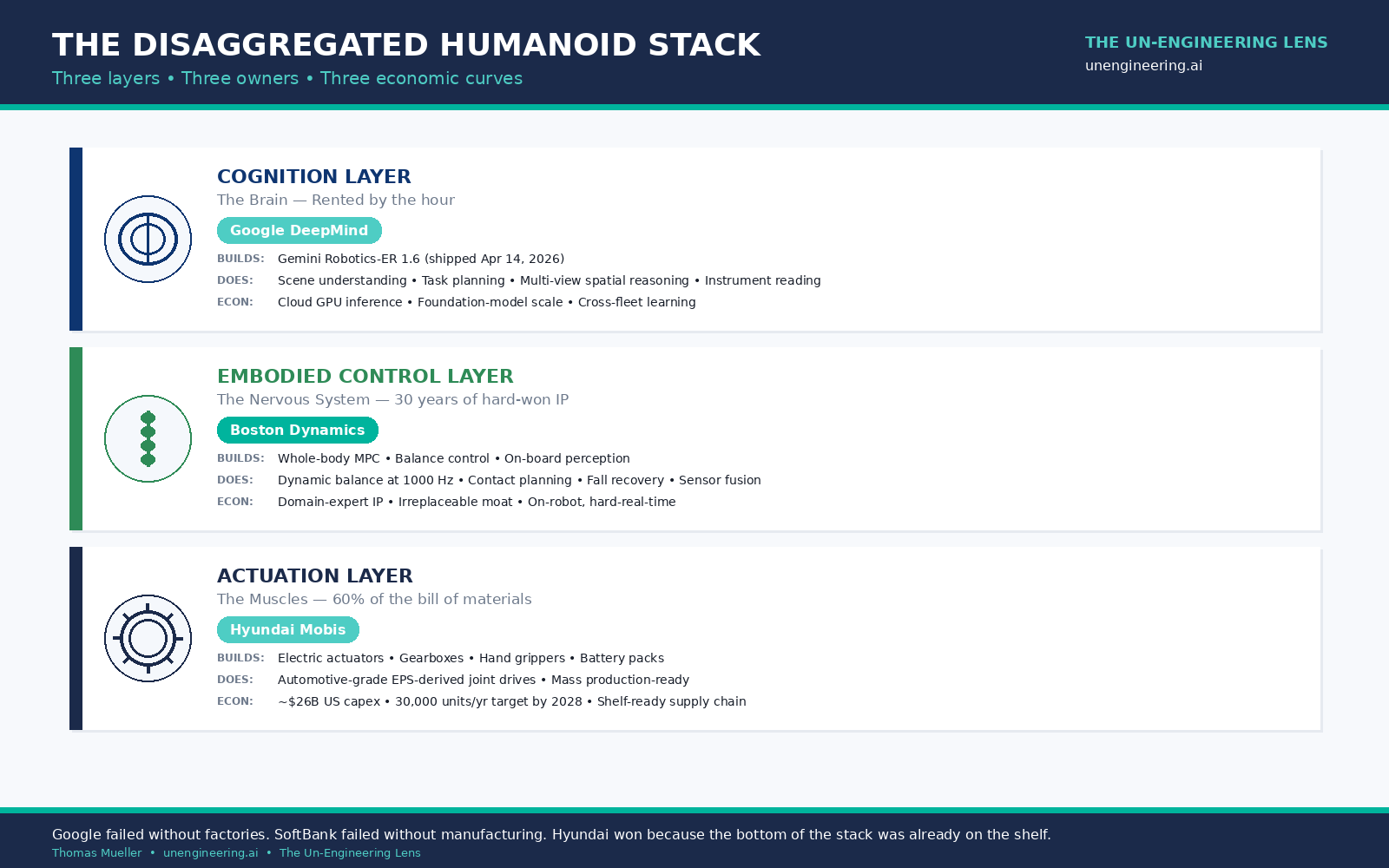

The lens: three stacks, three owners, three curves

The Un-Engineering reading of the Atlas announcement is that the production robot is a clean disaggregation of three previously-coupled things: cognition, embodied control, and actuation. Each of these layers is now owned by a different company, and each has a fundamentally different cost structure and scaling law.

Layer 1 — Cognition: the brain you rent by the hour

On April 14, 2026 — two days before I wrote this — Google DeepMind shipped Gemini Robotics-ER 1.6. It is what they now openly call a “high-level brain” for a robot: vision and spatial reasoning, task planning, success detection, and — critically — the ability to call tools. This is the layer that sits above a vision-language-action model and decides what the robot should do next.

This is not running on Atlas. It is running in a Google data centre. The robot is a thin-client. The brain is rented by the hour, priced on tokens and thinking-budget, and upgraded without the robot ever waking up from a battery swap. When a Gemini update ships in Mountain View, every Atlas in every factory in the world is smarter by morning. That is the foundation-model scaling curve operating on robot cognition.

The economics look nothing like a traditional robot controller. There is no per-unit cognition cost. There is a per-query cost, and it keeps getting cheaper as inference hardware gets faster and Gemini thinking budgets get more efficient. The cognition layer inherits the exact same curve that is currently compressing margins in cloud AI — only now the output is physical actions, not text.

Layer 2 — Embodied control: the nervous system you cannot buy

Below cognition sits the layer that makes a humanoid actually work: whole-body model-predictive control, dynamic balance, contact planning, impedance control, sensor fusion, fall recovery. This is the part that runs at 1000 Hz on-board, because the network will never be fast enough and the consequences of a delayed control loop are a broken robot and a lawsuit.

This is also the irreplaceable moat. Marc Raibert spent thirty years inside Boston Dynamics compounding the specific knowledge required to keep a two-legged machine upright under impact. DARPA alone directed roughly $200 million to that problem through the 2010s. Every humanoid startup that claims to “build their own walking stack” is either four years away or using an open-source reimplementation of the ideas Raibert’s team published a decade ago.

The economics here are the inverse of cognition. This layer does not scale with data centres. It scales with decades of engineering and a team you cannot hire because it does not exist yet. A competitor can reproduce a voxel graph in six months. Reproducing a production-grade whole-body controller from a cold start is a generational commitment.

Layer 3 — Actuation: 60% of the bill of materials

This is the layer that bankrupted the humanoid industry for a decade, and the one the entire sector still refuses to take seriously enough.

According to Hyundai Mobis, actuators account for roughly 60% of the material cost of a humanoid robot. That is not a rounding error. That is the whole economic problem. An industrial-grade actuator that can survive an 8– to 10-hour factory shift — with the thermal management, gearbox integrity, back-drivability and torque control that implies — is not a sensor or a chip. It is a high-precision mechatronic assembly. Building them by the millions, reliably, with automotive-grade quality, is a manufacturing capability, not a software project.

Hyundai Mobis has been building electric power steering assemblies at global scale for fifteen years. An EPS unit is architecturally close to a robot joint actuator — electric motor, planetary gearbox, torque sensor, controller — and Mobis already owns the automotive-grade supply chain to manufacture the components. At CES 2026, Mobis committed to supply the actuators for every Atlas that ships. This is not vertical integration on paper. It is vertical integration at manufacturing volume, already operating, already validated.

When Jaehoon Chang, Vice Chairman of Hyundai Motor Group, told the media that “actuators are the most critical hardware component that determines a lot of overall performance,” he was not being coy. He was describing the exact reason every competitor without automotive manufacturing heritage is currently stuck.

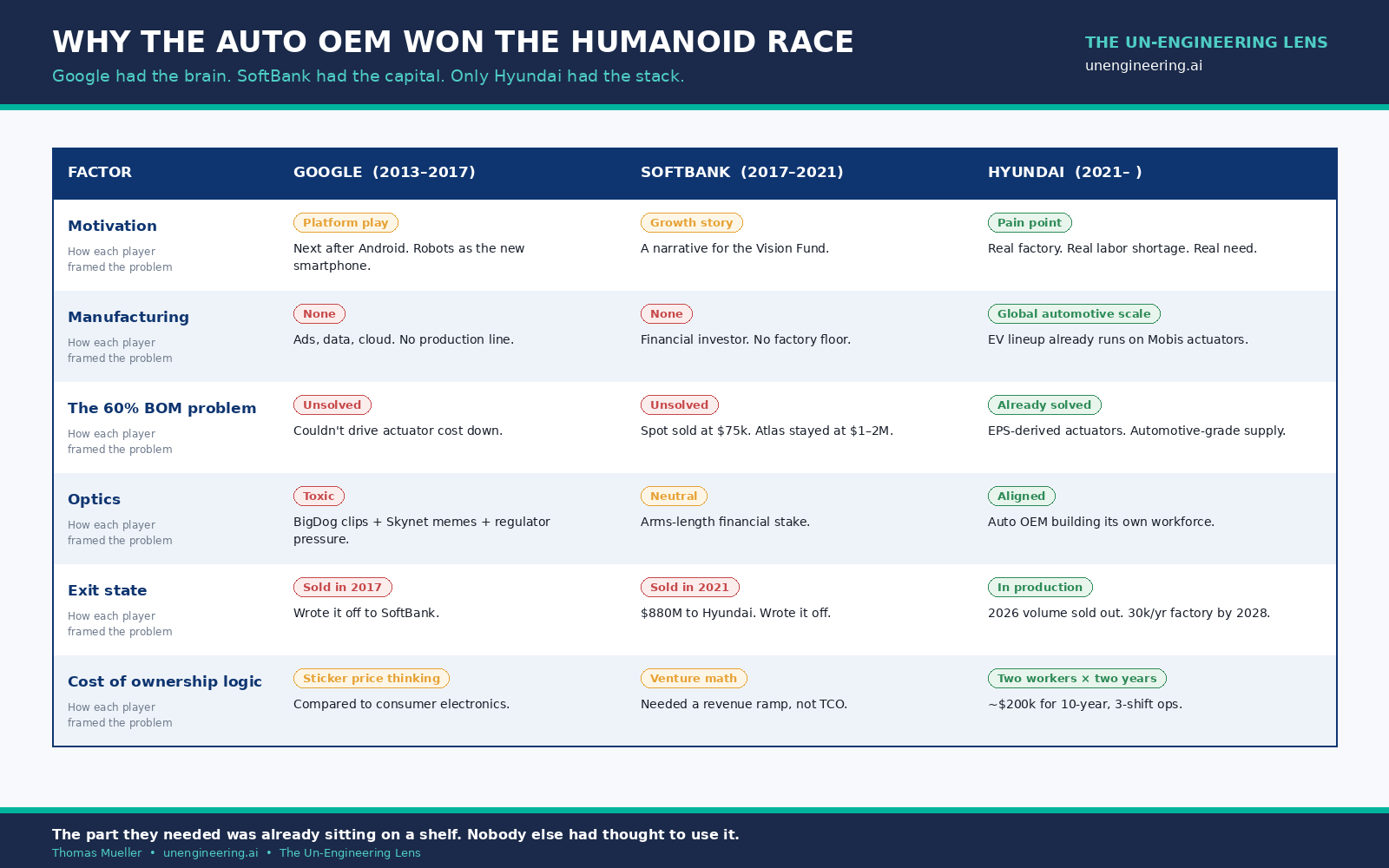

Why Google failed

Google bought Boston Dynamics in 2013 as part of Andy Rubin’s aggressive robotics shopping spree — Schaft, Industrial Perception, Redwood Robotics, and Boston Dynamics itself, reportedly north of half a billion dollars in aggregate. The thesis was straightforward: robots are the next platform after smartphones, and we are going to own the platform.

The thesis was also completely wrong for the asset. A platform play requires a product-scale manufacturing capability, a high-volume supply chain, and a business model that tolerates low per-unit margins at massive volume. Google had none of these things. Google has ads, data, and cloud. Google does not have a factory floor, and more specifically, Google does not have the automotive-grade component supply chain required to mass-produce the 60% of the BOM that is actuators.

Google also had an optics problem. The viral BigDog clips, the Skynet memes, and the regulatory environment around a search company owning a military-adjacent robotics division were genuinely difficult. But the optics problem was a symptom, not the disease. The disease was that Google wanted to own the whole stack and had production capability for exactly one layer of it — cognition — which, in 2013, was not ready. By 2017, Google had quietly sold to SoftBank.

Why SoftBank failed

SoftBank’s thesis was different and sharper, but the ending is the same. The Vision Fund playbook is to concentrate capital into companies that will own whole markets over a 30-year horizon — Uber, ARM, WeWork, DoorDash — and let the financial leverage compound. Boston Dynamics fit the narrative about intelligent machines perfectly, and the fund had the capital to wait.

To SoftBank’s credit, their pressure produced an actual product: Spot, a compact quadruped that shipped at roughly $75,000 per unit and is operating in more than forty countries today. That is a real result and it should not be minimised.

But Atlas stayed a laboratory installation. The hydraulic version ran $1–2M per unit and needed a full-time engineering crew to maintain. You cannot build a factory on that. You cannot build a business on it either. By 2021, SoftBank was exiting and Hyundai was buying.

“SoftBank knew how to write checks and wait for returns. Not how to run a factory floor.”

Why Hyundai won

Hyundai won because Hyundai did not have to own the whole stack. Hyundai only had to own the bottom of it.

When the Mobis-supplied electric Atlas replaced the hydraulic prototype, the cost envelope changed from “custom laboratory installation” to “automotive-grade component assembly.” Boston Dynamics kept the irreplaceable embodied-control moat. Google DeepMind provides the cognition layer as a foundation-model service. Hyundai Mobis handles the one thing that every other humanoid company is still burning cash trying to solve: industrial actuators at manufacturing scale.

Three layers. Three owners. Three economic curves stacked on one chassis. That is why the 2026 production run is sold out while competitors are still quoting twenty thousand dollar price points that assume actuator costs do not exist.

The total-cost-of-ownership math

Atlas is estimated to cost between $130,000 and $320,000 per unit. Tesla is still promising an Optimus at around $20,000. Unitree will sell you a smaller humanoid for around $4,000 today.

The buyers of the 2026 Atlas fleet did not care about the sticker price. They cared about TCO over a ten-year service life running three shifts a day without benefits, sick leave, or turnover. At the top of the quoted range, that works out to under $90 a day. No amount of Optimus’s promised $20,000 price will match that math unless Optimus also matches the payload, the reach, the dexterity, and the factory-floor reliability — all of which currently require actuators that Tesla does not manufacture at industrial grade.

This is what the industry keeps getting wrong about humanoid economics. The price of the robot is not the competitive variable. The cost of the actuators inside it is.

What this means for the rest of the field

If you are an operator

• Stop comparing humanoids on sticker price alone. Compare them on actuator provenance, service lifespan, and mean-time-between-maintenance on the joints that do the actual work.

• Ask where the cognition layer lives and who controls its update cadence. A humanoid running on a cloud-resident foundation model has a different risk profile than one running a fully on-board stack.

• Run a thin-client-plus-edge scenario against a fully on-board scenario. The economics diverge as the cognition layer compresses.

If you are a builder

• Your competitive question is no longer “can we build a humanoid?” It is “which layer are we building, and are we building it better than the automaker, the foundation-model lab, or the balance-IP incumbent who already owns that layer?”

• The middle layer — embodied control — is the highest-defensibility, lowest-reproducibility layer, and also the hardest to fund. Plan accordingly.

• If you do not have an automotive-grade actuator supply chain and you are claiming a $20,000 price point, you are making a margin bet that you cannot currently hedge.

If you are an investor

• The platform-play thesis that killed Google’s robotics division is back in venture decks under the label “general-purpose humanoid.” It is the same bet. It has the same economic flaw. The cognition layer is going to be dominated by two or three foundation-model companies. The actuation layer is going to be dominated by automakers. The gap between those is where a start-up can still build.

• Pay attention to Robotics-as-a-Service pricing as much as to sticker price. If the Atlas economic model lands, the per-hour humanoid becomes the comparable, and the startups pricing on per-unit logic will get repriced against it.

The lens forward

The humanoid industry spent the last decade arguing about whether it was a software problem or a hardware problem. The CES 2026 answer is that it was neither: it was a supply-chain problem dressed as a robotics problem, and only a company that already ran the supply chain could afford to solve it.

The next layer this thesis will reorganise is not humanoids. It is autonomous vehicles, Physical AI for industrial inspection, and defence autonomy. Each of those stacks is in the middle of its own cognition-control-actuation disaggregation right now, and each of them is about to discover that the hardest layer is not the one attracting the most venture capital.

That is the lens. When you see a platform play that requires owning three layers with three different economic curves, ask which layer the incumbent thinks it needs to own. Then ask where the other two already live. The answer is usually surprising, and it is usually already on somebody’s shelf.